New IDC Survey finds that only two-thirds of cloud service providers plan to have the same business model by 2020

SINGAPORE, August 23rd, 2018 – A new IDC survey reveals that cloud service demand due to Digital Transformation is changing the delivery of business-oriented solutions, with service providers ramping up their investments in new offerings to cater for their client's requirements not just for new infrastructure, but also applications, and managed and professional services delivered via cloud services. The survey finds that as a result, Asia Pacific excluding Japan (APeJ) services providers are rapidly exiting their traditional business models.

This is the first survey from the recently launched IDC Service Provider Pulse, the latest subscription service available from IDC Cloud Primary Research which provides a complete understanding of suppliers, buyers and consumers of cloud products and services across the entire ecosystem.

"Cloud service providers around the world are rapidly changing their business models in response to unprecedented customer demand, offering a mix of new cloud infrastructure, application, and managed services as part of an agile investment strategy," said Chris Morris, Vice President for Cloud Service Providers Research at IDC Asia/Pacific. "What is striking is not only the pace of transformation, but also the variety of offerings coming to market as a result. From managed cybersecurity to performance optimization, the hosting of complex business applications and hybrid cloud are offering the potential for service integration at point of delivery."

Highlights from the IDC Service Provider Pulse 1Q18 Quarterly Summary includes:

-

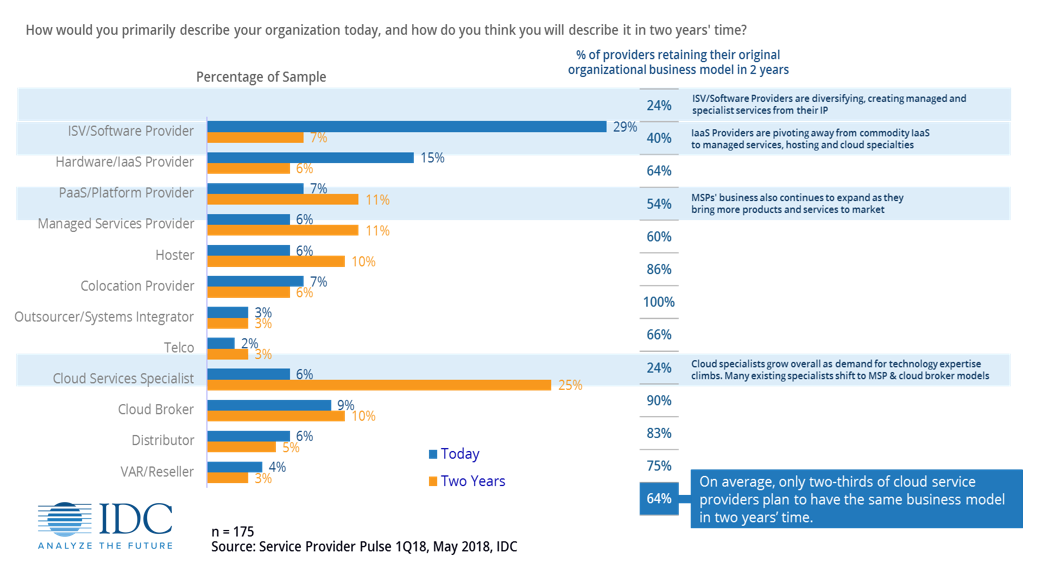

APeJ cloud service providers – including systems integrators (SIs), value added resellers (VARs) and distributors are dramatically shifting business models to managed services, PaaS & Cloud. On average, only two-thirds of cloud service providers plan to have the same business model by 2020.

-

Unsurprisingly, security is the most important consideration for 38% of cloud service providers to achieve their business goals in the next two years, while Security Services will account for the largest increase in new cloud service investment with 44% indicating that by 2020 they will bundling managed security services and professional services with their infrastructure service offerings.

-

81% of service provider revenues are for services above the infrastructure level, with opportunities existing in managed and professional services pulling-through demand for the underlying cloud services. Professional services are now a larger part of the revenue profile for smaller providers as they replace their traditional resale and hosting revenue streams with new managed services, while larger organizations are more focused on security services.

-

While resale of services from the hyperscale cloud SPs is common, maintaining control of their own IT is a key business strategy for cloud service providers with 69% planning to increase their level of spend on software, device, and/or IP development to better compete.

-

Software Specialists will increasingly become Services Specialists over the next two years, creating offerings usually associated with managed service providers, cloud service providers, hosting firms, telco providers, and outsourcers/systems integrators.

The IDC Service Provider Pulse is a quarterly survey using primary research from insights provided by IT business leaders and Line of Business executives with knowledge of their service strategy. The Q1 2018 findings are based on a May 2018 online survey of 500 respondents across North America, EMEA and Asia/Pacific. The IDC Service Provider Pulse is part of IDC's Primary Cloud Research product line that also includes CloudView, SaaSView, IaaSView, PaaSView and the Developer, and Managed CloudView surveys.

The data collection for the second survey has just been completed, with results to be published in September. This next survey answers questions such as:

-

Which infrastructure, application and managed services are driving service provider revenue?

-

Where will service providers invest for growth?

-

Which technologies will have the biggest - and least – impact?

Email Newsletters

Sign up to receive TelecomTV's top news and videos, plus exclusive subscriber-only content direct to your inbox.