Cloud-Native Telco: A DSP Leaders Report insights discussion

By Sean McManus

Jun 18, 2025

To embed our video on your website copy and paste the code below:

<iframe src="https://www.youtube.com/embed/H45d9pmp-FM?modestbranding=1&rel=0" width="970" height="546" frameborder="0" scrolling="auto" allowfullscreen></iframe>

Hello and welcome to TelecomTV. I'm Sean McManus, and today I'm hosting a panel discussion inspired by our latest DSP leaders publication, the Cloud Native Telco Market Perception Report. We researched how network operators view the clouds native telco sector. Although telcos are evolving towards cloud native infrastructure, they're not all moving equally fast and many different strategies are in play. Between April and May, 2025, we surveyed international network operators. Find out how vital native technologies are, how ready operators are to adopt them and who they trust to help. We had responses from 35 people, many of them senior level decision makers, representing more than 20, mostly tier one network operators. Between them, those operators have more than 1 billion customers. As a registered viewer of telecom tv, you can download the reports now for free. There's a link below this video if you're not yet registered, registration is free and gives you access to all of our reports and videos.

(01:33):

So please do go ahead and sign up. Joining me today to discuss the survey findings are Paul Miller CTO from Wind River, Robert Curran, consulting Analyst from Appledore Research. Beth Cohen, telco, industry Analyst from Luth Computer Specialists Inc and Mark Gilmour, Chief Technology Officer from ConnectiviTree Europe. Thank you all for joining me today. We've been following the progress of cloud's native telco infrastructure for years now, but how important is it really according to almost all of our telco executive respondents, the adoption of cloud native processes and technologies is either absolutely critical or very important to the future success of traditional telcos. So why is cloud native adoption so vital? Let's start with Paul on this one.

Paul Miller, Wind River (02:26):

Thanks, Sean. So pretty interesting response this time. You basically had 100% of the respondents placing cloud native as a critical technology for their networks, and we think we're really seeing this as a natural evolution of what's been having as most service provider networks have been transitioning to become software-defined entities. Obviously, years ago we had the early transition with any network functions, virtualization, which started with cloud computing in the core of the network using virtual machines. But as we now move to more modern implementations, we're leveraging Kubernetes and cloud native principles and containers since really 20 15, 20 16 timeframe as Kubernetes emerged as a modern technology. Now we're at a point in 2024 and 2025 where these things are battle hardened and proven and deployed at scale. And so as the natural evolution to software-defined networks happens across the entire service provider from core to edge and even IT and enterprise, back office, cloud native and containers, is the technology being used mass across all of those, across all of those areas. So naturally we're seeing the service providers indicate that that's a critical piece of technology as they look forward.

Sean McManus, TelecomTV (03:38):

Thank you, Paul. And what comments do you have to add, Beth?

Beth Cohen, Luth Computer Specialists, Inc. (03:42):

I'll build on what Paul said, and I think the operators and particularly the large ones, took advantage of the cloud native technology when rolling out the 5G technology because we had to start from scratch. So that was a good opportunity to really do a full tech refresh and using cloud native services and cloud native approaches was really the way to go, and it has proven to be very cost effective and been very to the telco operators that did take that approach.

Sean McManus, TelecomTV (04:29):

Thank you, Beth. Robert, let's hear your view on why cloud native adoption is so important.

Robert Curran, Appledore Research (04:35):

Yeah, I think obviously both Paul and Beth have painted a picture there of the technological trends underneath. I think it comes down to what's most important for operators, and I think what we're seeing now is the realization that for the kind of flexibility and scale and agility that they want, that they were promised with virtualization and promised with 5G, those things were incomplete in themselves. And actually unless you go cloud native on the core applications and from a architectural point of view, you won't get that overall end-to-end scale and agility. So I think that's why it's so important looking forward. I'm not surprised that your respondents to the survey have been pretty positive about it as a direction that's going to allow telecom to gain these qualities that's been talking about for a while. This is really an essential ingredient

Sean McManus, TelecomTV (05:26):

And Mark, let me bring you in there.

Mark Gilmour, ConnectiviTree (Europe) (05:29):

Well, really just to add that this cloud native architecture is kind of a fundamental building block for the things that we want to do future wise when we talk about an AI native environment or API driven or high levels of automation, really this all requires the building blocks of a cloud native architecture to offer that flexibility, offer that scalability that we need going forward.

Sean McManus, TelecomTV (05:58):

Thanks everyone for those opening comments. Let's now move on to the next data point. Cloud native is clearly an essential strategic development for telco operators, but are they already from an operational and cultural point of view to adopt cloud native processes and technologies? Not everyone thinks so. In fact, 63% of our respondents think only a few operators are ready. What's holding back the telco community? Why are they not all ready for this critical transition? Robert, why don't you start us off?

Robert Curran, Appledore Research (06:35):

Yeah, I think with a few different factors involved here. The first is that this is really very different and involves investment in additional skills and expertise. That's something that perhaps bugs weren't really budgeting for planning and expecting, and obviously it's skills that come from outside of the telcom industry to some degree. Even where we need a combination of skills is definitely something that's extra coming with any change, talking with any kind of change is obviously something of a challenge. So I think telcos are trying to make this evolve along this path of cloud native, which is actually quite a revolutionary change. I think there's a little degree of just friction in the process. Everyone can see that it's the right way to go, but they're trying to juggle managing the business, managing current networks with this evolution, attract the right skills, learn as they go along.

(07:30):

I think there's another factor in here, which is relatively speaking, I think relatively few peer company references. We all know we're still at quite an early stage in this journey. There are some good proof points to start with, but it's still not yet at the level of seeing an obvious peer company doing so much better in the market as a result of going cloud native. So you've got a mix of different factors in here. Folks are trying to make progress along the right lines, but it is challenging, it is difficult, it is new and it's going to take some time.

Sean McManus, TelecomTV (08:02):

Thank you. Beth, what would you say are the challenges holding up cloud native adoption?

Beth Cohen, Luth Computer Specialists, Inc. (08:07):

I would say building on what Paul said, the cloud native does require a different perspective and a way of thinking that I think a lot of the network engineers that are traditionally have traditionally worked in telcos took a while to adopt. I mean, my personal experience was when I introduced some early cloud native products a few years ago, I had to explain virtualization networks and how all of that stuff worked and their sort of lock in on, oh, it's a piece of hardware, was something that I had to break them of that idea in their head. Now, I believe, and I do know that they did get past that they're smart people and I think that certainly in my experience, that many of the operators have gotten over that hump and do understand the basic concepts of virtualization and cloud native and of course containers and network segmentation and all those technology approaches that are needed to really adopt the cloud native, cloud native infrastructure. I think where we're falling down is in the CICD end of things, the DevOps approach, and now we're getting hit with AI and how to incorporate that in as well. So it's a continual challenge to adopt cloud native because the technology is rapidly evolving and the telco engineers have to speed up and stay current.

Sean McManus, TelecomTV (10:05):

Brilliant. Thank you. Mark, did you want to come in with some points on this?

Mark Gilmour, ConnectiviTree (Europe) (10:09):

Yeah, it's almost like compound change. I think we're asking a lot of our teams right now within the telco industry. So this move is compounded by all the other moves coming on top of that, whether it's automation, whether it's like Beth just mentioned a kind a DevOps CICD approach to operations, and that's a culture change. That's a culture challenge. Robert hinted towards that as well. So I think these are some of the reasons that are affecting or slowing that progress, but we have one or two, well more than one or two operators that are really leading the charge there and the rest of the industry will follow along and has to follow along in order to maintain that kind of capability going forward.

Sean McManus, TelecomTV (11:09):

Thank you, Mark. And finally for this question, Paul, let's hear from Wind River.

Paul Miller, Wind River (11:13):

Yeah, I think we have a bit of a global perspective here, and if I had answered this question a couple of years ago, I would've absolutely biased towards the skills and expertise, right? The challenge within the service provider of having trained personnel that are skilled in IT and enterprise technology like Kubernetes and data center architectures and software defined networking. That was definitely a vacuum a few years ago. But I do think, and Beth is correct, we've kind of moved beyond that As we look in North America, we have Verizon and Boost with hugely scaled cloud native networks, Vodafone in the UK and moving to other European regions, followed closely by Arran and Telefonica and Deutsche Telecom in Japan, we have KDD and NTT Doomo moving along quite well. So I think we're starting to see some pretty significant global adoption. So the real challenge here is no longer technology.

(12:02):

I think it's really around things like TCCO and business justification. I think service providers are concerned as they move to this technology, is it going to be equivalent or cheaper than what they're currently doing with an appliance-based approach? Equivalently, some operators include in their TCO analysis, the idea of forward-looking revenue generation. As you move to a more software-defined, if you will, cloud-based architecture or to edge in your network, you have more flexibility to launch more services. You no longer have to ask a telecom equipment manufacturer, can I run X application on your box? Right? Because you now own the cloud infrastructure core to edge, and that then factors in and creates a motivation for some of the early movers to become the first carrier in their region to be able to launch these new services and generate revenue often at the expense of their rivals. So I do think there's some business and some maturity, business maturity factors here that are driving certain operators to move quickly and other operators to move slower, but no longer so much driven by technology readiness.

Sean McManus, TelecomTV (13:05):

Thank you, Paul. Lots of differing views and challenges for the telco community to consider there. Let's move on now. The transition to cloud native is only possible with the support of the vendor community. So is the tech supply side ready to help operators become cloud native? According to the majority of our respondents, only a few specialist vendors have the skills and know-how to properly help telcos. Why hasn't the broader telecom vendor community stepped up? Robert, let's start with you for a broader perspective on this one.

Robert Curran, Appledore Research (13:40):

Yeah, I was a little surprised at your survey findings there. I think they're a little harsh on the vendor community, if I'm honest. I think there's still an issue if you don't know what you're looking for, it's going to be difficult to know when you found it. And I think that there's still a bit of, notwithstanding what Paul said about some of the reference examples that are there, I think the majority of telecom, it's still a little unclear what it's aiming for. And so when it goes out to look at the market, guess what? It doesn't exactly find it. I think that's what the survey is really reflecting rather than a reality of where the vendor community is. I think the vendor community has gone quite a long way in general. I think there are vendors out there, clearly Wind River is one, there are others as well who have made a lot of progress on Cloud native and over quite a long period of time as well.

(14:30):

So I think that is there. I think there's another factor in here that telcos do need to recognize is that I don't think the market is going to move ahead of them. They need to invest. If they want cloud native and they want the agility and they want the business benefits and innovation that Paul's referenced, they have to be prepared to invest in it and not wait for the vendor community to come with an answer and then buy two or three or four years down the line. I don't think that's going to work in this case. So I think, as I say, I think the survey response have been a little harsh on the vendor side, but at the end of the day, the market will respond if they can see that there's a market opportunity and money to be made, the vendor community will up its game even further. But tele have got to meet the vendors halfway I think.

Sean McManus, TelecomTV (15:13):

Thank you. Let's hear from Mark next on this.

Mark Gilmour, ConnectiviTree (Europe) (15:16):

I think if we broaden the definition of telecom beyond the cellular world and expand out a little bit more, I understand this, the results on this survey question a lot more because as many are aware that the area where I now operate in with connectivity is actually in the wholesale fixed market, and there it's a little more difficult to get the vendor community to move in the cloud native, a truly cloud native, cloud native first environment. What I've tended to see is appliances that have been cloudified stuck in a virtual machine or something like that, but not really made that full transition has happened more substantively in the ran side of things or the cloud bio two edge as Paul mentioned. So I think there's more to do in that space. Just to give a point on this, I had a requirement to kind of build a digital twin version of my optical network. And actually because of the way the appliances are built at the moment, it actually was more cost effective for me to just buy some tin and build the lab that way rather than build it fully virtualized in a cloud environment. So there's still some way to go, but again, it's kind of different segments of the market, different segments of the telecom industry.

Sean McManus, TelecomTV (16:55):

Interesting. So let me bring Beth in there. Beth, what would you like to add?

Beth Cohen, Luth Computer Specialists, Inc. (17:00):

So I want to pick up on a number of points. So one is the telecoms have always been kind of loathed to, they're great at creating requirements, but they're not always great at communicating them. And I think that there needs to be more dialogue between the vendors and the telecom people to really move it forward. So I think that's definitely contributing to the problem. And I think there's another factor which is that established vendors, that's always the entrepreneur versus the established vendor dynamic, which is that established vendors have a huge base that if they bring out a new product that literally eats into their base, that's a problem for them. So I think Wind River and Rakuten and some of the other up and coming vendors that don't have that long legacy of building hardware, and there's one vendor in particular, which I will not name, which is no matter what they say, they're still basically selling boxes. And I think they have to get out of that mindset before really getting to where they need to be. And I don't think the telecom community, the telecom operators are forceful enough with these vendors to say, Hey guys, we're not going to just keep buying your boxes if you don't get with the program.

Sean McManus, TelecomTV (18:46):

Thank you. And Paul, let me bring you in for Wind River's perspective on this.

Paul Miller, Wind River (18:51):

Yeah, so I guess we're a guilty participant being one of the vendors here. I'd really classify the response to this question with two kind of topics. One is around innovative is dilemma, and the other is around ecosystem. And so one of the problems here in under adoption as relates to Innovator's Dilemma is you have incumbents versus innovators, right? And as Beth described, the incumbents have a tremendous huge business here. They have the ability to sell the hardware, the services, the support, the incremental software upgrades. They own the entire value chain, right from that legacy if you will, 4G timeframe where everything was sold as appliances. As you move to a more cloud native architecture, it breaks apart the business model. You now have off the shelf server providers, you have virtualization providers such as ourselves. Then you have the telco incumbents now relegated to just providing, if you will, just the application layer functionality.

(19:49):

That's the telco function that breaks apart the business model. And so the incumbents are very resistant to that. So you have those legacy incumbents that are moving slow as Beth described, and then innovators such as Wind River, as we've seen Samsung and Avenir and others use that paradigm as a way to leapfrog their competitors, right? And we'll talk later about how some Wind river's done some of that, but that creates interesting innovators dilemma dynamic and that causes the market to be fractured as we go through 5G. Now, as we go to six G, we think we'll be fully adopted into a cloud native environment, and that will be the exclusive way that that technology is deployed. So once you go past Innovator's Dilemma, then we talk about ecosystem. And one of the challenges that comes with the great benefits of a disaggregated network is now you have multiple vendors coming into your network and you have to integrate them. And so the real success comes from those vendors that work together outside of the customer environment and fully integrate their solution. So the customer still perceives a high quality solution that they can deploy at lowest their network. If a vendor is less skilled in that ecosystem participation and they enter and force the customer to integrate in their environment, there's high costs and complexity and delay to market. So effectively those two sources, the Innovator's Dilemma problem and the ecosystem problem have created some of this paradigm.

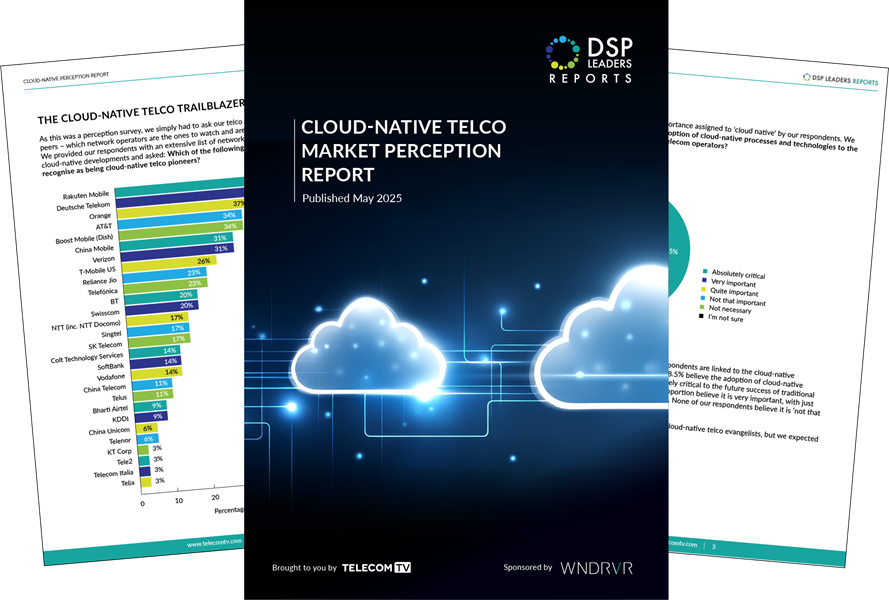

Sean McManus, TelecomTV (21:10):

And again, Paul, thank you for rounding out those final thoughts for us on that question. Now with every transition, there are always some companies that lead the way. Our telecom operator executives identify Japan's Recruitin mobile and Rakuten Mobile, and two European telco giants, Deutsche Telecom, and Orange as the top three telco trailblazers. In your view, is this top three a fair reflection of industry developments? Beth, let's start with you.

Beth Cohen, Luth Computer Specialists, Inc. (21:41):

I don't think it is because I do know Verizon's down at 31%. Verizon's been innovating in this area for at least a decade, if not more, and it just doesn't brag about it, doesn't talk about it much. So I know there are other telecom operators that just, it's part of their ecosystem, it's their infrastructure. It's not particularly customer facing and I don't think it's going to move the needle and their stock price, so they just don't talk about it. But they're definitely doing it because it drives costs down, it drives innovation, it drives new products, so it drives efficiency. So I would say far more telecom operators are doing it than is perceived.

Sean McManus, TelecomTV (22:39):

Thank you. Paul, what do you think? Is this top three a fair reflection of the industry?

Paul Miller, Wind River (22:44):

I think it all comes from your perspective and which carriers familiar with. Certainly different international regions may be only familiar with their region as they respond. As we look at the market globally, we see, for example in Japan, KDDI and in particular NTT Doomo with our friend of beta san very public about what they're doing with open ran and cloud native infrastructure. We see in the UK in particular, Vodafone very advanced in deployment and certainly as Beth mentioned, Verizon and also of course, boost in the United States with the world's largest open ran network, fully deployed on a cloud native architecture. Telus and Canada, the first adopter there. So I would've filled it out a bit differently if we're coming from a cloud native perspective looking at what's happening globally with carriers. But we do know that, for example, orage is very active in Silva, right? As a cloud native European principle being used in Europe. So again, I think it depends on your perspective, but I probably would've filled that out a bit differently.

Sean McManus, TelecomTV (23:47):

Thank you. Let's say your perspective, Robert.

Robert Curran, Appledore Research (23:50):

Yeah, I think like the other panelists here, I think it's a kind of yes or no answer if I'm honest. I think it's a fair affection among the people who are clearly leading and have been for a while in setting the pace and sharing a lot of information. I think in looking at the results you have, I think some of the operators are a bit underrepresented. I know there's a lot of good work going on among Chinese operators, particularly work at scale, and they're not quite so public, perhaps not quite so accessible, but certainly we had some access to some of what they're doing in there. It's pretty interesting. And looking further down the list, some of the Nordic countries or companies like Swisscom, you look at Tel Orelia, Eliza, they're all very pioneering in some of the work that they're doing. So I think there's more work that's going on in some of these companies. Perhaps on your survey really reflects.

Sean McManus, TelecomTV (24:37):

Thank you. Let's now come to our final talking point for today. Every vendor wants to be regarded as a market leader. It's interesting that the vendors seen as the cloud native telco leaders are not those normally associated with telecom network infrastructure. It's also worth noting that when we did our first cloud native telco markets perception survey in late 2023, neither Wind River nor Rakuten Symphony were in the top six names. Now they're in positions three and five respectively. While Avenir has risen in the ranks from sixth last time to fourth this time, what do these results tell us about cloud native telco trends? Let's start with Mark.

Mark Gilmour, ConnectiviTree (Europe) (25:22):

Well, I think it tells us that there's an opportunity here for alternative vendors, particularly in the RAN and the core space, or that that ecosystem is broadening when you look at those top three, for example. But I'll let Paul comment, sure, he'll have a good comment to make on that about being represented there. But you look at those top three and they're about providing the infrastructure, providing the services, providing the wraparound to go with that as well as not just the actual, the software, the appliance as it were now. So I think there's a great opportunity. I think what we do see is that currently it is biased towards the cellular part of a telco's portfolio, and that resonates quite well because that's where we've been seeing most of the development in cloud native approaches for the telco market. So I think those are some of the takeaways I would see from that survey.

Sean McManus, TelecomTV (26:37):

Thank you. Let me bring Paul in next on this then Paul, what would you add?

Paul Miller, Wind River (26:41):

Well, certainly we were very pleased as a company to see our finish here and really honored that the customer would put us there. So thanks to everyone for that. It's really the result from our perspective of six or seven years of really hard work, blood, sweat and tears, pretty significant investment into cloud native infrastructure. You do notice, of course in the survey a mix of the application vendors such as we were discussing as well as the cloud technology vendors, red Hat and AWS and Wind River in here. I think that speaks to the criticality when you see the top three finishers being cloud native infrastructure providers, the criticality of that cloud native technology, right? That foundational element that you need in the network to support the applications that we've been talking about. I also think our rise over the past several years has been our focus and investment in cloud native technology. We've been a new open source founder in the Starling X initiative, which is the most modern cloud native and distributed cloud capable system that you can purchase today anywhere in the world. And then finally, one of the reasons that we've rose is we're actually beating the top list names here regularly in business. Some pretty famous events have happened recently with our boost win in the United States as well as others internationally. So again, we're very, very proud and honored that the customers would select us for their networks and really looking forward to the future.

Sean McManus, TelecomTV (28:06):

Thank you. Beth, let's hear your views on this, please.

Beth Cohen, Luth Computer Specialists, Inc. (28:09):

I think there's a number of factors, and I think some of it ties into the Innovatives dilemma that we talked about earlier, that the new entrants have the most powerful thing an entrepreneurial company has is a blank piece of paper, which the more established players don't have. But I think there's also that the telcos themselves are thinking out of the box far more and are open to we're going to do business with a variety of players, not just the ones that we've been doing business with decades. I do want to have a comment about the providers. AWS and Google are both mentioned, and I know Microsoft has had a big push, although I guess they dropped in the ranks for whatever reason, and there's been a big push by the CSPs to onboard the telco infrastructure onto their platforms, and I think there's been some mixed results on that, and that probably is reflected in the survey results as well.

Sean McManus, TelecomTV (29:30):

Thank you, Robert, let me bring you in on this, please.

Robert Curran, Appledore Research (29:34):

Yeah, just a couple of fairly obvious points I think is some of the other panelists have referenced here under the banner of Cloud native, it's clear we've got an ecosystem here. These top five companies, four of them do different things. So when operators are thinking about what cloud native means, it's not any one company. It's a range of companies. So we're back to the idea that the idea that this is an ecosystem is taking hold, which is necessary and absolutely correct. I think it is also interesting by extension that the traditional telco vendors don't feature so strongly in here. There's progress being made in there, but clearly in the customer's minds that the affinity just isn't as anything like as strong compared to some of the newer players or the newer entrants into this space. I think that's interesting. I think just, I put a word of caution in here.

(30:25):

The recognition is not what drives revenue. What drives revenue is that this matters to customers and our customers customers, and I think that's something that we still have work to do as an industry to prove that this has value, not just for the technological sake, but because it makes a real difference to business perform. It makes a real difference to innovation and services, and as Paul referenced earlier, that there's upside to going cloud native. It's not just about rearranging what you already do, it's about doing things in a new way, a way that has value to your customer and value to your business. I think that's still a fight that we still have to work on for sure, and keep pressing home the advantage of Cloud Native.

Sean McManus, TelecomTV (31:04):

Unfortunately, we are going to have to wrap up this discussion there as we have run out of time. Thank you to our panelists for your comments and insights and remember to download the DSP Leaders report for the full data and analysis. It's available to all registered viewers of telecom tv, and as I said at the start, registration is free and grants you access to all of our videos and reports. So please do go ahead and register. Thank you for watching and goodbye.

Please note that video transcripts are provided for reference only – content may vary from the published video or contain inaccuracies.

Panel discussion

This panel discussion, hosted by TelecomTV’s Sean McManus, looks at the findings of the Cloud-Native Telco Market Perception Report. Experts from Wind River, Appledore Research, Luth Computer Specialists and ConnectiviTree explore the importance of cloud-native technologies for network operators, the readiness of the telecom sector for this transition, and the role of the vendor community in supporting this shift. The dialogue underscores the strategic imperative of cloud-native adoption for the future success of telcos.

Featuring:

- Beth Cohen, Telco Industry Analyst, Luth Computer Specialists, Inc.

- Paul Miller, CTO, Wind River

- Mark Gilmour, Chief Technology Officer, ConnectiviTree (Europe)

- Robert Curran, Consulting Analyst, Appledore Research

Sponsored by ![]()

The Cloud-Native Telco Market Perception Report - published May 2025

The Cloud-Native Telco Market Perception Report is a 13-page editorial publication that provides a snapshot of how network operators view the progress of the telecom sector as it adopts cloud-native processes and related technologies.

The report is based on a survey, conducted in April and May 2025, of network operator executives (including multiple CXOs) from around the world who represent companies, from Tier 1 multinational operators to challenger regional service providers, with a combined user base of more than 1 billion customers.