Datacentre M&A heading for another record year

By Ray Le Maistre

Jun 29, 2022

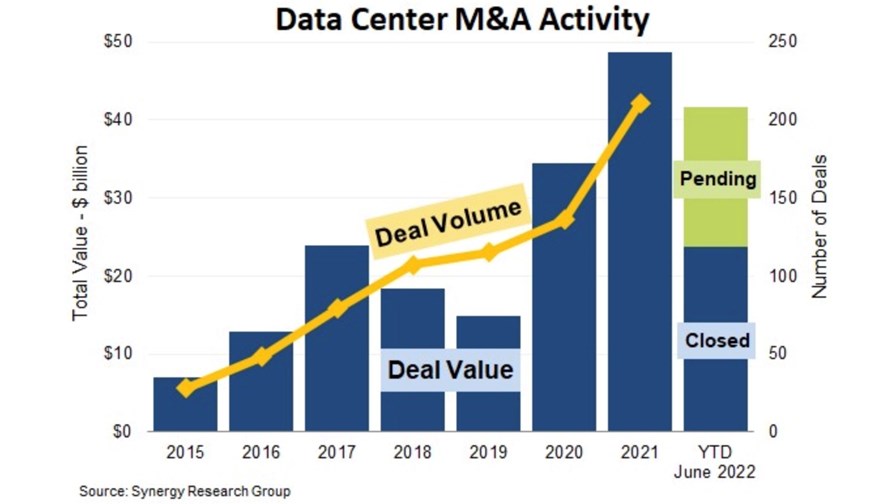

- In the first half of 2022, 87 datacentre M&A deals have already completed

- Synergy Research team has identified more that are soon to close

- Value of full-year datacentre M&A could top 2021’s $48bn total

- Private equity funds now playing a much bigger role

This year is shaping up to be another record one for datacentre merger and acquisition (M&A) activity, with 87 deals worth some $24bn already having closed during the first half of 2022 and an additional $18bn in pending deals set to close, according to the team at Synergy Research.

“After adding in the regular flow of transactions that happen with little advance public notice, 2022 is shaping up to match the record-breaking M&A activity levels that were seen last year,” notes the research firm.

In 2021, there were 209 deals with an aggregate value of $48bn, up from $34bn in 2020 (see chart, above). “The highlights for this year have been the $15bn acquisition of CyrusOne by investment firms KKR and Global Investment Partners, and the pending acquisition of Switch by DigitalBridge for $11bn. The 2021 highlights were the acquisitions of CoreSite and QTS, each for around $10bn. These deals represent the four highest-value acquisitions the industry has ever seen,” noted the Synergy Research team in this press release.

The research firm also highlighted that an increasing proportion of datacentre M&A deals now involve private equity firms. “A notable trend in the industry has been the recent influx of private funds. In the 2015-18 period, private equity buyers accounted for 42% of deal value. Between 2019 and 2021, as the overall level of M&A activity ballooned, private equity share of the total deal value increased to 65%, while in the first half of 2022 private equity share has jumped to over 90%,” the press release noted.

The rapid growth of the cloud services sector, the “aggressive expansion” of the hyperscale giants – Alibaba, Amazon Web Services (AWS), Google Cloud, Microsoft Azure, Tencent and more – and the increasing use of data-rich digital services are all contributing to increasing demand for datacentre capacity which, in turn, is driving up the investment value of the facilities, notes John Dinsdale, chief analyst at Synergy Research Group.

“Building and operating large fleets of datacentres is highly capital intensive. Even the biggest data centre operators have had to seek external funding to allow them to meet growth targets while protecting their balance sheets. As the level of resulting M&A activity has shot through the roof, virtually all of the incremental investment has come from private equity,” explained Dinsdale.

- Ray Le Maistre, Editorial Director, TelecomTV

Email Newsletters

Sign up to receive TelecomTV's top news and videos, plus exclusive subscriber-only content direct to your inbox.