Bring on the unified digital support system

By Ian Scales

May 30, 2024

- Could digital support system solutions be the next generation of OSS/BSS without the ‘BS’?

- We can’t promise that

- But it does look like the best bet for a more coherent future

With senior executives from the telecom industry having clearly identified the development of next-generation telecom software solutions as one of the most important areas of technology development over the next three years, TelecomTV recently hosted its inaugural Digital Support Systems (DSS) Summit to discuss the prospects for a unified, cloud-based OSS, BSS and associated technology stack.

The general industry consensus going into the summit was that the development and deployment of digital support system (DSS) solutions should be a key goal for communications service providers (CSPs) and their tech suppliers since it would lead to better management and network capabilities, greater efficiencies and would boost CSP progress on their quest to becoming full digital service providers (DSPs).

The overriding question was: “What’s the preferred tech route?”

Like all such quests there were a range of mild disagreements about the best way forward and the summit did a good job of surfacing these for discussion, but – spoiler alert – the less tractable issue concerned the merits and demerits of cloud-native processes and the use of public cloud platforms. Do we need to push doggedly forward with both?

Backstory

It’s hard to overstate the importance of what, despite its legacy nature, the industry still often calls operational and business support systems (OSS/BSS). Tacked onto the edge of the telco technical estate, their original role was to ‘support’ human efforts to troubleshoot and manage the network then tot up the customer bill. These systems tended to be fragmented and run in IT silos and were inevitably inflexible, and expensive to implement and maintain. As a result, they jacked up the cost of operations and the ordeal of transitioning from one technology to the next as the telco services themselves became more complex.

As a result, instead of always easing network transitions and enabling telco planners to make the most of their new technologies, the shortcomings of the siloed environment, with its overlapping technologies, tended to act as a drag anchor on telco business development.

An extreme example of pre-computer OSS/BSS inflexibility was still on show in the early 1990s when I attended a walk-through tour of one of BT’s last operational mechanical (Strowger) exchanges in the UK. Chunky bindings of copper cable ran everywhere and a giant lead acid battery bigger than a hot tub had been installed somewhere under banks of clickety clanking mechanical switches. But the standout revelation was the billing system. It involved a large board on the wall with an array of mechanical meters – one per subscriber – each one counting the talk-time ‘units’ for the calls made through the switch via a cam which rotated to tick over the units for the meters, speeding up at ‘peak’ periods. At a designated moment, a photographer appeared with an impressive, modern camera (about the only modern thing in the building) to snap the board for the humans to calculate the subscriber bills.

Although ingenious, simple and presumably reasonably reliable, this ‘system’ was utterly inflexible and couldn’t fold in new services or requirements – in effect, a switching technology first developed in the final years of the 19th century had effectively limped into the digital age to sweat the final few million billable local call minutes before, finally, being swapped for a phalanx of digital cabinets.

While today’s telecom systems and subsystems are now close to being all-digital and software-controlled and are, therefore, theoretically more adaptable (no more timing cams or mechanical meters!) the problem of managing and transitioning OSS/BSS support for successive generations of telecoms technology is still a real issue and has arguably become more difficult the more complex services have become.

What’s to be done?

Bring on the holistic, fully integrated, unified digital support system! During our summit, it was generally agreed by the panellists that an integrated next-gen DSS for telcos was the missing ingredient in the DSP recipe and its development should proceed as quickly as possible.

“We’ve ended up with a spaghetti of systems,” said John Abraham, principal analyst at Appledore Research but, our experts agreed, the code operating in the core is not monolithic and every CSP is on its way towards a unified system, which should provide significant advantages.

“For instance,” noted Beth Cohen, SDN network product strategy at Verizon Business Group, “unification means we can offer better SLAs [service level agreements]. Being able to automate SLA credits – a really costly activity – would be a big win for the telcos.”

This unified system would have to be ‘holistic’ in scope, requiring not just things like call time recording (as in the case of our Strowger billing example) but an ability to measure, respond and orchestrate by drawing in a range of near real-time data streams and pertinent state information to make timely decisions in pursuit of things such as call rating, security, power saving, latency optimisation, failback options, and much more: Ongoing network performance improvement and assurance, not to mention an ability to use the DSS to help squeeze network power consumption, would all rely on it.

Boiling this down, a DSS must be cloud-based, dynamic, de-siloed and highly integrated, thus capable of gathering and correlating both network and business data to deliver valuable insights into both business strategies and operational management. But can the available technology and software deliver on this ambition? After all, gathering data inputs is one thing – processing them to come up with decisions (in near real-time in some instances) is quite another.

This is often where the need for AI rears its familiar head. Buoyed by advances in generative AI, many in the industry are confident that they can see an AI light at the end of the fibre; others caution that it will take a little time.

Verizon’s Cohen was adamant: “Generative AI is still not to be trusted,” she said, and it has a long way to go before it can be.

So where does that leave the prospects for a transforming DSS?

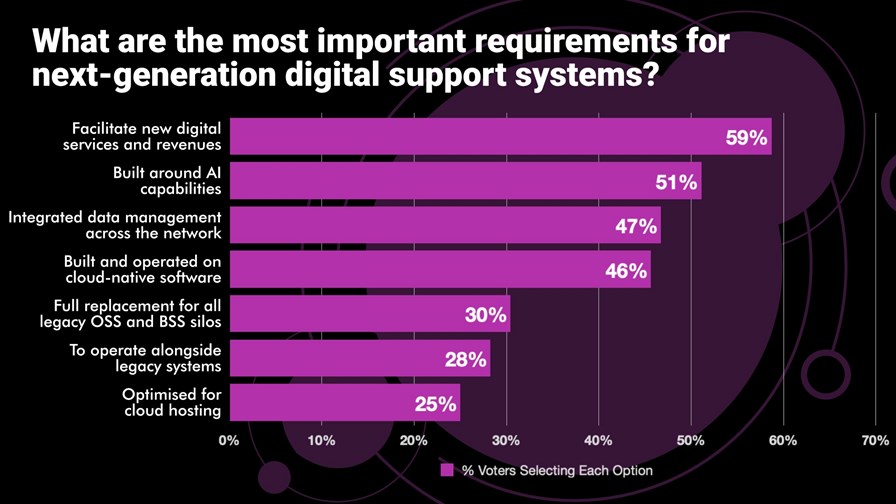

In development with much work still to do, if sentiment measured on the day is anything to go by. As we always do with our summits, we conducted a survey asking what viewers thought were the key requirements for next-generation digital support systems, the results of which can be found in this article and in the graphic below.

The results showed a lack of consensus about the best way forward.

For instance, only 25% of our survey respondents thought optimising the systems for cloud hosting was important, but at the same time 30% favoured the replacement of all legacy OSS and BSS silos with next-generation digital support systems, while 28% thought next-gen solutions should operate “alongside” the legacy OSS/BSS applications.

The last two requirements aren’t necessarily contradictory – a transition to cloud-native software implies that at least some ‘legacy’ systems would have to operate in parallel for a period, after all. But they do indicate a tension around opposing concerns: On the one hand recognising the practicalities of the transition, on the other, understanding that the advantages of an effective and unified DSS may be compromised if legacy OSS/BSS functions are retained as part of the mix.

Cloudy thinking

The biggest issue, judging by the summit Q&A session, was that while there appeared to be a good level of acceptance that the DSS should be cloud native – for the flexibility, application interworking, partner integration etc – opinions were divided over the optimum telco cloud partner strategy. What circumstances favoured either private cloud, hybrid cloud, multicloud or public cloud?

“I would say that multicloud is very much the order of the day,” noted TM Forum EVP for member products and services, Andy Tiller. “All the bigger operators are working with all the hyperscalers, not so much to hedge their bets as to take advantage of the different capabilities that each of those partners provides,” he said.

But while the major operators appear to be interested in staying loose and diversifying their partnerships to optimise their workloads, extract savings and increase their capabilities, the traditional OSS/BSS integration pendulum may be swinging back in the opposite direction for many players in the Tier 2, 3 and MVNO end of the vendor market, according to Amir Mehmood, director of solution engineering at Optiva.

He claimed he’d detected a marked trend for OSS and BSS vendors to focus on pre-integrated solutions – where the applications, such as billing, inventory or field force automation etc, are sold and supported as an integrated suite – “often from a single vendor and hosted on the one cloud,” he stated.

Even so, most operators, especially the Tier 1s, “aren’t on a mission to integrate all their OSS/BSS,” claimed TM Forum’s Tiller, who said that while there had been a lot of workload offloading to the cloud, these arrangements were generally not exclusive.

Tiller pointed out that the OSS/BSS pendulum has spent at least 20 years swinging back and forth between “pre-integrated” and “best-of-breed” approaches. Having the flexibility to swap pieces out one at a time is clearly very attractive, so what the industry really needs, he said, was “easily integrated best of breed” (EI-BoB?). Fixing on cloud native as a preferred environment would arguably make for easier software integration (and disintegration), no matter which cloud ‘type’ was chosen.

So how might this work?

The TM Forum’s original mission was to provide a framework for telcos to describe (in tortuous detail) their business processes and a ‘taxonomy’ (a standard set of names) for those processes.

For the most part, the TM Forum approach wasn’t to collectively micromanage the exact nature of each process but to foster a common language and understanding of what was being developed by each member ‘under the hood’.

A telco’s (or OSS vendor’s) process map might then form the basis for internal training, strategy discussions and technical engagement with suppliers, partners and customers. From there, the forum went on to help telcos map their process steps into their OSS/BSS applications leading eventually to it developing a ‘composable digital architecture’ (CDA). This, claims Tiller, might help create a composable software ecosystem for next-gen OSS/BSS. “Easily interworked best of breed”, perhaps?

But which cloud type?

Cloud partnering for telcos is not just about the specific benefits on offer by a cloud partner but about getting access to cloud skills, best available via the hyperscalers and the effective use of AI. Tiller pointed out that while the hyperscalers can channel the software development effort on their own platforms using a relatively coherent set of tools and frameworks, telco infrastructure has tended to diverge.

“Therefore, in TM Forum we’re very keen to encourage the industry to ‘go cloud native together’, rather than everybody doing their own flavour,” he said, pointing out that the hyperscalers “had tens of thousands of developers all working to the same standards and approaches, while in telecom all the systems had been built by many different parties. So if everyone goes about their cloud migration in their own way, it will lead to a lot of customisation and a large future legacy to maintain.”

That might suggest that the public cloud (or clouds) was the overwhelmingly obvious choice for telcos looking for a strategy for their next-gen digital systems hosting rather than them all doing their usual thing of forging incompatible environments.

However, Lingli Deng, research director at China Mobile, maintained that going cloud native does not necessarily mean “that we have to move to a public cloud deployment pattern.”

She said telcos needed to choose between public, private and hybrid deployment patterns according to their requirements, especially when taking into account things like national data regulations.

Where did the summit leave us?

Once again, a TTV summit highlighted the importance of scale in telecom, or at least the need to hitch a ride with a partner or alliance that has it. On that basis ’public cloud native’ was odds-on favourite to lead the charge.

One thing might be clear: The idea that the AI-driven, automated, next-generation system should continue to be viewed as a ‘support’ system for humans will become totally outmoded.

One way or another, the DSS will be merged with the network core and assisted to some degree by AI. When that’s achieved, we’ll see a complete inversion of the old support system concept, with switching, transmission and billing being the systems that support the DSS, not the other way around.

- Ian Scales, Managing Editor, TelecomTV

Email Newsletters

Sign up to receive TelecomTV's top news and videos, plus exclusive subscriber-only content direct to your inbox.