Making those IoT connections: low power, low cost = high growth

By Ian Scales

Jun 2, 2016

")

via flickr © Lisa Brewster (CC BY-SA 2.0)

Ericsson’s Mobility Report is out and, as usual, it presents a wealth of detail on what’s growing and what’s growing, but not quite as fast. Smartphone subscriptions are still a big deal and, when the numbers are all in, the booming smarties are forecast to have passed ‘basic’ phone subscriptions in Q3 this year. Yes, we all thought they’d already done that, but that’s growth curves for you. And the smartphone will sail on and on, nearly doubling in subscription terms by 2021 when today’s 3.4 billion subs will have turned into 6.3 billion globally.

Not only will the number of smartphones out there keep growing, so too will the average amount of data up- and downloaded per phone. That dynamic will be in part driven by a “dramatic shift in teen viewing habits,” claims the report, which estimates that the use of cellular data for smartphone video grew 127 per cent in just 15 months (in 2014-15) while between 2011 and 2015 there has been a 50 per cent drop in the time teens spend watching TV/video on a TV screen and an 85 per cent increase in those viewing TV/video on their smartphones instead.

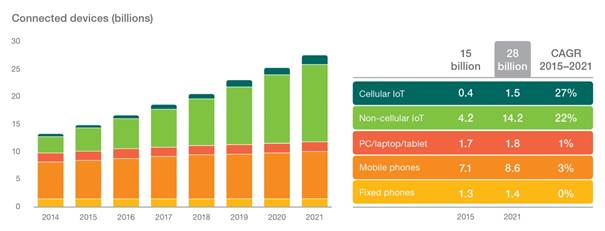

But all that smartphone growth appears somewhat pedestrian in comparison to what’s brewing up in the IoT world. In the report Ericsson chose to lead (as we press types say) with the assertion that between 2015 and 2021, the “number of IoT connected devices is expected to grow 23 per cent annually so that of the 28 billion total devices that will be connected by 2021, close to 16 billion will be IoT devices,” and the vast majority of those will be ‘non-cellular’.

Satisfying growth, but at what price?

Source: Ericsson Mobility Report

In the figure above we can see the dramatic impact those ‘non-cellular’ IoT connections can have on a stacked bar chart - take out that green component in the middle of the bars (in your imaginations) and you’re left with a very slight incline rather than what looks like the beginnings of a hockey stick curve.

The truth is that connections growth will have a dramatic effect on the industry’s bar charts and growth curves, but not anything like as much impact on things like revenues and data loads.

In terms of connections the ‘non-cellular’ IoT - WiFi, unlicensed LPWAN and any connection that doesn’t involve a cell SIM - will see the bulk (14.2 billion) of connection volume over the chosen time period of 2015 - 2021. Cellular IoT, on the other hand, will enable 1.5 billion connections by 2021. That’s still a substantial number and Ericsson sees SIM connections capturing most of the really valuable IoT applications where latency, reliability, data speed and interactivity (between cloud and remote device) are important.

But the big connection numbers obviously belong down at the low end where devices will run over WiFi connections (and therefore offer little if any value to network service providers) or over low-cost LPWANs which will be dirt cheap - that, after all, is the whole idea.

One of the big news items this week in IoT was ‘non-cellular’ LPWAN deployer, Sigfox’s, plan to have its one-way, low-speed LPWAN up and running across 100 of the largest US cities this year (see SIGFOX hooks up with Atari to plot mass market IoT devices).

Sigfox’s connections, designed to pass very short coded messages to remote devices, are targeted to be priced at around $1 per year (in bulk). That’s a large order of magnitude less than your typical annual smartphone subscription. Clearly we need a new way to quantify our ‘mobile’ and wireless segments.

Email Newsletters

Sign up to receive TelecomTV's top news and videos, plus exclusive subscriber-only content direct to your inbox.